Crossover Investing: What is it and who does it? Simply put, crossover investing is late-stage private investing in companies who plan to access the public markets through an initial public offering (“IPO”) within approximately 12-18 months. By definition, the crossover round is expected to be the last private round of financing before a company goes public. Crossover investors are typically entities that are public-market investors who have the experience, expertise and relationships to participate in venture round financings.

The Crossover Round: A stop on the biopharma IPO roadmap. Crossover investors often later participate in that company’s IPO. This can be favorable for company management teams, as prior participati0n by public market investors can lend credibility to a company’s market acumen as well as support the IPO through insider participation. In addition to lending clout, crossover rounds also increase the likelihood of a company going public and typically result in larger financings. From mid-2020 to early 2021, private companies that went the crossover route were 4x as likely to go public and had final private round raises that were almost twice the size of non-crossover companies that later went public1.

Why the Biopharma Sector? Biopharma companies are prime candidates for private funding to support the cost of therapeutic clinical trials, which typically increase in scale and cost as pipeline candidates navigate the approval process through the U.S. Food and Drug Administration. As an illustration of the popularity of crossovers, in 2021, there was $21 billion in total U.S. private biotech money raised and over 80% of biopharma IPOs were preceded by a crossover (2020), up from just over 40% in 2017.2,3

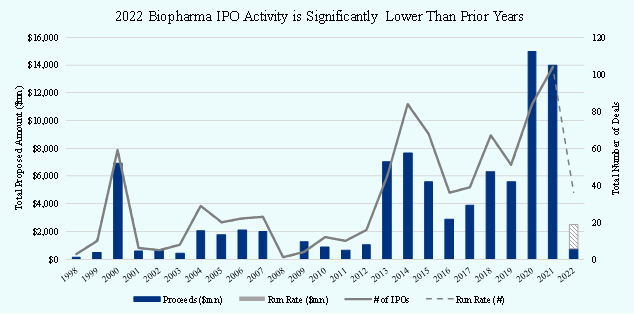

Why Participate? Arbitrage. Since 2014, the increase in valuation from the last venture round to IPO (step-up) has been 1.6x in the biotechnology space4. We believe this valuation arbitrage will persist due to limited competition in the crossover segment. In fact, we would expect higher step-ups for companies that access the capital markets in 2022, similar to the trend witnessed in early 2017, given currently highly depressed biotech valuations. As a result of these dynamics, we believe that managers who are seasoned crossover investors and poised with the right industry relationships are likely to continue to see a swell in their pipeline of candidate companies seeking private financing. If current trends continue, we believe this acceleration of private deal activity and demand could likely persist for the remainder of 2022 and into 2023. Values will likely be found over the next 12 months, in our view. As depicted below, IPO activity has all but halted during the first half of 2022, increasing the list of potential private transactions. Further, we believe existing venture investors, board members, and management teams will be much less price sensitive to valuation talk and term sheet economics than in recent years.

Crossover Investing: An advantage in diligence. From an investor perspective, crossover investing provides an opportunity to evaluate a company and its management team over a longer timeframe than the typical investment bank driven, test-the-waters period preceding an IPO. We believe that crossover investing is particularly intriguing within biopharma as the clinical trial process, by its nature, is a high stakes/high reward proposition. The insight gained from investing in the last private round can allow for intensive due diligence over the 12-18 months before IPO. In addition, crossover round investing often comes with board participation or observation rights, which can provide an additional level of insight into a soon-to-be public company. From a financial perspective, private companies that complete a crossover round typically have higher step-up multiples at the IPO and better post-IPO performance5.

Scarcity: Hard transactions to source, limited real players. We believe that the competition investing in the biotechnology crossover market is limited, as most firms usually focus on either private or public investing, and typically don’t have expertise in both, which we believe is critical given these private investments often aim to complete an IPO and become publicly traded within a year. We believe the biopharma space clearly favors healthcare sector specialists due to the complex diligence needed for biotechnology companies.

Why now? Valuations are compelling. The biotech market has been severely out of favor since it peaked in the winter of 2021. We have seen the SPDR S&P Biotech ETF (the “XBI”) lose greater than 47% of its value in this timeframe6. Given the current market dynamics, the cadence of deal flow has ground to a halt. There were only 12 crossover financings in the first quarter of 2022 and none in the month of March – marking the first month with zero crossover activity since May 2018.2 For comparison, the first quarter of 2021 saw 40 crossover deals.2 IPOs have seen a similar slow down with only 5 year to date.7 Further, many of the companies who completed an IPO in 2021 are trading well below their IPO valuations.7 Despite the challenging public and private markets, biopharma companies continue to operate and, as such, will continue to need funding.

About us:

Clough Capital Partners L.P. (“Clough Capital” or the “Firm”) is a global multi-strategy alternative asset management firm founded in 1999 and based in Boston, MA. We employ fundamental research to invest in public and private markets, across various asset classes and manage an array of strategies for our clients.

BILL WHELAN | Partner

Bill Whelan joined Clough Capital in 2014 and has over 16 years of experience in the investment management industry. Prior to joining the Firm, Bill was an Investment Principal at Partners Capital, a private investment office focused on multi-asset class investing, from 2010 to 2014. Previously, Bill was an Equity Research Analyst at Millennium Management, a multi-strategy hedge fund, from 2008 to 2009 and at Fidelity Management and Research from 2005 to 2008. Bill earned a B.A. in economics from Harvard College.

NOELLE TUNE, M.D.| Director

Dr. Noelle Tune, M.D., joined Clough Capital as a Director in 2020 and has over 22 years of healthcare investment and industry experience. Prior to joining Clough Capital, Noelle worked at a major urban medical center in the Boston area as an emergency medicine physician and continues to practice medicine. She completed her residency at Indiana University, where she served as a Chief Resident in her final year of training. Before entering medical school at the University of North Carolina at Chapel Hill, from 1999-2005, Noelle worked at Leerink Partners (now SVB Leerink) covering specialty pharmaceuticals, biotechnology and healthcare services. Noelle then started her own private label research offering through Soleil Securitas. Noelle earned a B.A. in Russian and Soviet Studies from Harvard University. While at Harvard, she was captain of the women's rowing team and currently serves as a Director for the Friends of Harvard and Radcliffe Rowing.

*In polling for the ‘Best of Boutiques’, Institutional Investor asked analysts and portfolio managers at asset management and hedge funds to name the boutiques or regional firms that they believed had done the best research work over the preceding 12-month period in each of the industry and macroeconomic categories polled in the All-America ranking. Scores were produced by weighting the number of votes awarded to a firm based on the size of the voting institution. The rankings were determined based on the numerical score each firm received.

Disclosures

1 Source: Torreya Life Sciences Venture Equity Market Review from June 2021, CapitallQ and Crunchbase, including global life science companies and deal sizes >$25m between June 2020 and March 2021. Approximately 484 private rounds included in universe. Clough Capital did not invest in a majority of companies included in this data.

2 Source: SVB Biopharma Crossover Summary from March 2022 and company reports

3 Source: Locust Walk Crossover Evolution report from March 2021, Pitchbook, including biopharma IPOs from 2015 to 2020 with and without crossover rounds, excluding raises <$20M and when IPO was >12 months from last private round of financing.

4 Source: Bank of America Merrill Lynch, VentureSource, and issuers’ S-1 filings as of 1/20/2022. Includes all SEC registered, US-listed healthcare IPOs with post-greenshoe deal sizes >$50m and excludes re-IPOs and companies that did not conduct a mezzanine financing round within 18 months of IPO. Approximately 347 IPOs included in universe. Universe of multiples is used for informational purposes only. Clough Capital did not invest in a majority of companies’ IPOs that are included in this chart. Step-up multiple at IPO price represents the IPO valuation price divided by the previous financing round valuation price. Step-up multiples do not necessarily correlate to profits, which may or may not ever be realized, including due to pre-IPO shares being subject to contractual lock-up terms for a period of time following a company’s IPO.

5 Source: www.forbes.com/sites/brucebooth/2014/11/07/the-biotech-cross-over-phenom-biomarker-ofquality

6 Source: Bloomberg. The SPDR S&P Biotech ETF is an exchange-traded fund that seeks to replicate the performance of the S&P Biotechnology Select Industry Index, an equal-weighted index that represents the biotechnology sub-industry portion of the S&P Total Markets Index. The S&P Total Markets Index tracks all the U.S. Common stocks listed on the NYSE, AMEX, NASDAQ National Market and NASDAQ Small Cap exchanges. The performance of the index referenced herein is used for information purposes only. One cannot invest directly in an index.

7 Source: Bloomberg and company filings. This document has been prepared by Clough Capital. Although not generally stated throughout, the information in this document is the opinion of Clough Capital, which opinion is subject to change and none of Clough Capital, its affiliates or any funds or products they manage shall have any obligation to inform you of any such changes. This document is not an offer to sell, nor a solicitation of an offer to buy any security in any fund managed or sponsored by Clough Capital or any of its affiliates, or any other investment product or security. Offers to sell or solicitations to invest in any funds may be made only by means of a prospectus or confidential offering memorandum, and in accordance with applicable securities laws. Prospective investors should review the prospectus confidential offering memorandum for any funds before any investment is made (including, without limitation, the information therein with respect to investment strategy, conflicts of interest and risk factors). This document has been prepared from original sources and data believed to be reliable. However, no representations are made as to the accuracy or completeness thereof and neither Clough Capital nor any fund shall have any obligation to update this document at any time thereafter. Strategies highlighted or discussed in this document do not represent an entire portfolio. There can be no assurance that the strategies discussed herein have been or will be profitable or that similar investment opportunities will be available in the future. Nothing in this document shall constitute a recommendation or endorsement to buy or sell any security or other financial instrument referenced in this document. This document includes forward looking statements, including projections of economic conditions. Neither Clough Capital nor the any funds or products they manage make any representation, warranty, guaranty, or other assurance whatsoever that any of such forward looking statements will prove to be accurate. There is a substantial likelihood that at least some, if not all, of the forward-looking statements included in this document will prove to be inaccurate, possibly to a significant degree.